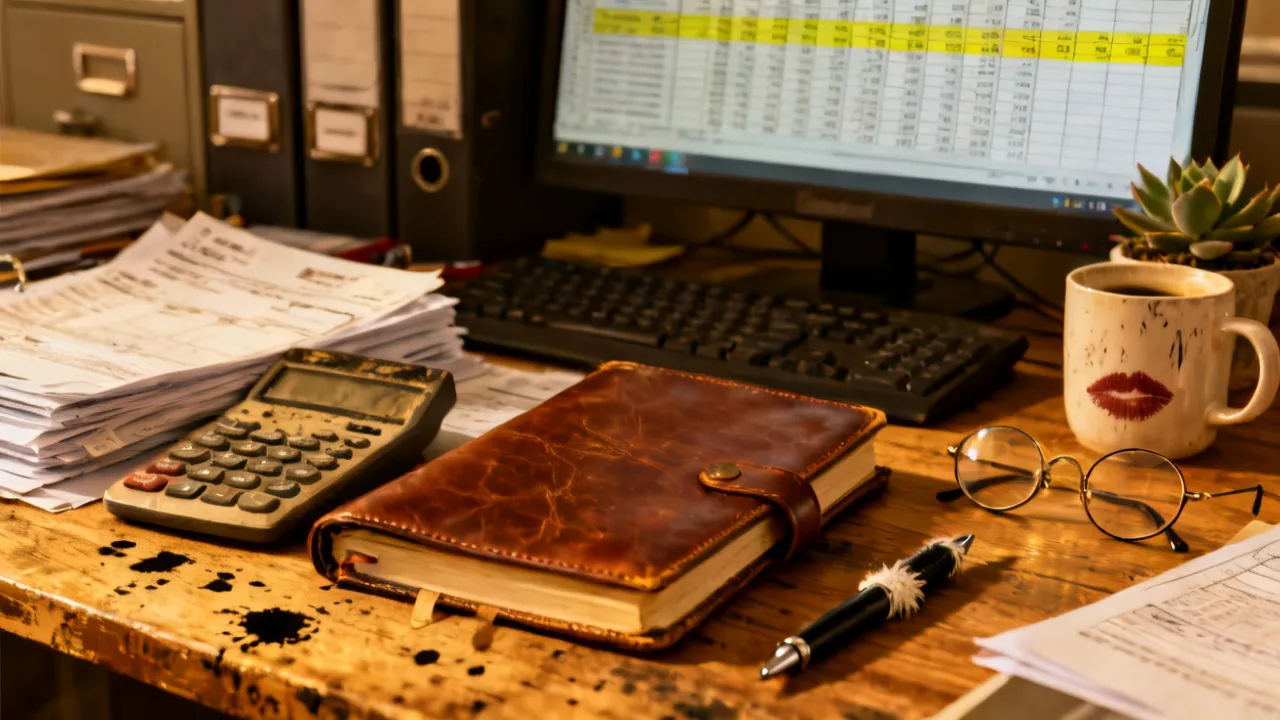

Bookkeeping is a vital part of any business’s financial health, ensuring accurate recording and analysis of financial transactions. This guide provides an in-depth look at the safe keep of an entity's financial records, offering insights from industry experts. Discover the essential practices, methods, and modern tools that streamline this critical financial process.

In the world of business, bookkeeping plays a pivotal role as the backbone of financial management. Accurate bookkeeping is crucial for companies, whether large or small, ensuring that financial records reflect true values, supporting decision-making processes, and ensuring compliance with relevant laws and regulations. The primary aim of bookkeeping is to systematically record all transactions affecting the financial position of a business, providing insights into the entity's financial health. This foundational practice not only facilitates the day-to-day operations of a business but also sets the stage for its long-term strategic planning and growth.

Effective bookkeeping can lead to a better understanding of a company's financial status, which aids in identifying trends, forecasting future performance, and making informed decisions. Thus, investing time and resources in establishing a robust bookkeeping system can yield dividends in the form of clearer financial visibility and increased operational efficiency.

1. Recording Financial Transactions: The initial and very critical step involves documenting every financial transaction. This includes sales, purchases, receipts, and payments, along with more intricate details like payroll expenses, taxation, and other financial obligations. Each entry should be recorded with specific details such as dates, amounts, parties involved, and the nature of the transaction to ensure clarity and completeness.

This meticulous documentation is not merely a record-keeping exercise; it is a vital component of strategic planning. Regular analysis of these records allows businesses to gauge their financial progress and make informed decisions regarding investments, budget allocations, and operational adjustments.

2. Ledgers and Journals: These are the traditional tools used to categorize and organize transactions. Journals offer a chronological log, facilitating easy tracking of financial activity over time, while ledgers classify transactions into specified accounts—such as assets, liabilities, equity, income, and expenses—creating a structured and accessible record. Each account in a ledger corresponds to a specific aspect of the company's financial activities, providing a granular view of its monetary position.

These tools are not outdated; in fact, they have evolved significantly with technology, creating enormous efficiencies in how businesses maintain their financial records. Digital ledgers and journals in accounting software eliminate manual errors and ensure instant accessibility to financial data.

3. Double-Entry System: This method, known for its efficiency, requires each transaction to be entered as both a debit and a credit in separate accounts. This dual approach not only preserves the accounting equation (Assets = Liabilities + Equity) but also serves as a check against errors. If the sum of debits does not equal the sum of credits in the books, it indicates a discrepancy that requires correction. This system enhances accuracy and offers a comprehensive overview of a company’s financial activities.

Moreover, the double-entry system empowers businesses to track the impact of transactions more effectively, providing insightful reports that can influence operational strategies and resource allocations.

4. Trial Balance: This report, produced periodically, proves the arithmetical accuracy of ledger accounts. It helps detect errors promptly and is instrumental in preparing financial statements. A well-prepared trial balance serves as a checkpoint, identifying discrepancies before the final accounting statements are produced. It acts as a diagnostic tool to ensure that the books are balanced and ready for further analysis.

As technology advances, bookkeeping has significantly evolved from manual processes to digital solutions, allowing for greater accuracy and efficiency. Several software options enable streamlined accounting, real-time reporting, and vast integrative capacities with other business functions. Notable among these are QuickBooks, Xero, and FreshBooks, which offer user-friendly interfaces, making them favored choices for contemporary businesses.

These platforms not only automate many of the tedious aspects of bookkeeping but also enhance functionalities such as invoicing, expense tracking, and financial reporting. They provide features that allow users to produce real-time financial reports, forecast future performance, and identify potential financial pitfalls before they escalate.

| Tool | Features | Top For |

|---|---|---|

| QuickBooks | Comprehensive financial tracking, customizable reports, payroll management with robust customer support. | Small to medium-sized enterprises looking for extensive functionality. |

| Xero | Real-time data, inventory management, integration with over 800 apps, user-friendly for collaborations. | Growing businesses with international operations needing real-time visibility. |

| FreshBooks | Time and expense tracking, invoicing, project management, particularly suited for service-based businesses. | Freelancers and small business owners looking for simplicity and efficiency. |

With these advanced tools, businesses can collect data in real-time, which boosts financial analysis and strategic planning capabilities. The integration of artificial intelligence and machine learning into bookkeeping software promises even greater advancements, such as predictive analytics for financial performance and automation of complex tasks that previously required human intervention.

Despite the benefits of modern tools, businesses still face common bookkeeping challenges:

Industry experts emphasize several top practices to enhance bookkeeping efficacy:

Moreover, understanding the business model and its operational intricacies enables bookkeepers and financial managers to tailor their approach effectively, ensuring that the bookkeeping practices align with the company’s goals and strategic vision.

Q: Why is bookkeeping important for small businesses?

A: Bookkeeping provides small businesses with accurate financial information critical for strategic planning and decision-making, ensuring tax compliance and facilitating access to funding or investment opportunities.

Q: Can I handle bookkeeping myself or should I hire a professional?

A: While software tools make it easier for small business owners to manage bookkeeping, hiring a professional can provide expertise, efficiency, and ensure compliance, especially as a business grows. A professional can also offer insights that may not be visible to a business owner handling bookkeeping independently.

Q: What is the top bookkeeping method for startups?

A: The double-entry bookkeeping system is generally recommended for startups due to its thoroughness and accuracy. It allows for a complete understanding of the startup's financial position and helps in identifying trends over time.

Q: How often should financial statements be reviewed?

A: Financial statements should be reviewed monthly to ensure up-to-date financial health assessments and inform strategic decisions. This regular review allows businesses to react proactively to changing financial conditions or operational challenges.

Q: How can businesses improve their cash flow through better bookkeeping practices?

A: Implementing timely invoicing, closely monitoring receivables, and maintaining comprehensive records of expenses and cash flow can drastically improve cash flow management. Additionally, budgeting and forecasting based on financial data can enhance the planning process, enabling better financial decisions.

In conclusion, effective bookkeeping is integral to business success, providing a clear view of financial health and supporting strategic growth initiatives. By understanding and utilizing top practices and modern tools, companies can enhance accuracy, improve compliance, and achieve good financial stability. Bookkeeping is not just about maintaining records; it is a crucial aspect of financial management that empowers businesses to thrive in today’s competitive environment. By investing in robust bookkeeping systems and practices, businesses set the foundation for growth, sustainability, and long-term profitability.

Furthermore, as we look towards the future of bookkeeping and financial management, the integration of technology will continue to redefine how businesses manage their finances. Keeping abreast of these developments and adapting to new tools and regulations will ensure both efficiency and compliance in an evolving marketplace. As businesses prioritize effective bookkeeping, they enhance their potential for success and become adept at navigating the intricate world of finance.

Striking the Perfect Balance: Navigating Premiums and Out-of-Pocket Expenses in Senior Insurance Plans

Explore the Tranquil Bliss of Idyllic Rural Retreats

How to Make Lasting Memories at Disneyland Attractions

Affordable Full Mouth Dental Implants Near You

Unlock the Top Kept Secrets to Finding Your Ideal Dentist for Flawless Dental Implant Results!

Discovering Springdale Estates

The Guide to Car Trading

Unlock the Full Potential of Your RAM 1500: Master the Art of Efficient Towing!

Understanding Royal Canin Maxi Adult

Understanding Compliance and AML Strategies

This article delves into the intricate realm of Compliance and Anti-Money Laundering (AML) strategies, highlighting their significance in the corporate world. Compliance AML refers to the organizational adherence to legal standards and regulations to deter financial crimes, ensuring transparent and ethical financial practices. This comprehensive guide examines these strategies' complexities and their pivotal role in safeguarding economic integrity.

Exploring B2B MBA Opportunities

Dive into the dynamic world of B2B MBA programs, designed for professionals seeking to enhance their strategic and management skills in a business-to-business context. This comprehensive guide discusses the significance of B2B MBAs in today's market, highlighting how these programs equip leaders with the expertise to navigate complex B2B relationships and drive business success.

Understanding Whitewater Regenerative Blowers

Whitewater Regenerative Blowers are essential in various industrial applications for their efficiency in moving air and gases. These blowers are known for their durability and ability to operate continuously, making them a preferred choice for industries ranging from wastewater treatment to aquaculture. This article explores their features, benefits, and applications, offering readers a comprehensive understanding of their importance in modern industry.

Mastering Employee Retention Strategies

Employee retention has become a critical aspect of organizational success, particularly in the dynamic landscape of 2020. As businesses strive to maintain a stable and productive workforce, understanding effective retention strategies is essential. This article delves into key methods for enhancing employee satisfaction and retention, offering a comprehensive guide for HR professionals and business leaders alike.

Discover the Allure of Splendys

Splendys stands as a beacon of innovation and style within the consumer goods sector. Known for their commitment to quality and style, Splendys products range from luxury apparel to sophisticated home decor with a modern twist. Their unique offerings cater to discerning customers seeking both function and aesthetics, positioning Splendys at the forefront of contemporary design excellence.

Understanding Headhunter Ti Services

This guide delves into the role and effectiveness of Headhunter Ti in the recruitment industry. Headhunters are specialized recruitment professionals who seek out top talent for specific job roles, often for high-level or specialized positions. This article provides an in-depth analysis of how Headhunter Ti operates, its benefits to organizations, and what candidates can expect when engaging with such services.